Buying your first home in Ottawa can feel exciting, overwhelming, and honestly a little intimidating all at once.

Between rising home prices, mortgage rules, down payments, closing costs, and figuring out where you actually want to live, there’s a lot to navigate. I work with many first-time homebuyers across Ottawa, and one thing I hear constantly is:

“I just don’t know where to start.”

The good news is that buying your first home becomes much easier once you understand the process step-by-step. In this guide, I’ll walk through what first-time buyers in Ottawa need to know before purchasing a home in Ontario.

Step 1: Start With a Mortgage Pre-Approval

Before looking at homes, the smartest first step is getting a mortgage pre-approval in Ottawa. A pre-approval helps determine:

- How much home you may qualify to buy

- What monthly payments may look like

- What mortgage programs fit your situation

- Whether you need to improve credit or reduce debt first

- How much down payment is required

- Whether you can lock in an interest rate early

What Impacts Your Mortgage Approval?

Several factors affect how much you qualify for:

Income — Employment income, salary, hourly income, bonuses, self-employment income, and other sources all matter.

Existing Debt — Car loans, student loans, credit cards, lines of credit, and other monthly obligations reduce borrowing power.

Credit Score — Better credit often creates more lender options and stronger rates.

Down Payment — Your down payment can significantly affect both affordability and available mortgage products.

Step 2: Understand Ottawa Down Payment Rules

In Canada, minimum down payments are generally:

- 5% on the first $500,000

- 10% on the portion between $500,000 and $1,500,000

- 20% minimum over $1,500,000

Why 20% Makes a Difference

Once you reach a 20% down payment, you move into what’s called a conventional mortgage, which can open up a few additional options. Most notably, you avoid paying mortgage default insurance, which can significantly reduce your overall borrowing cost. In some cases, you may also have access to longer amortization options, depending on the lender and property type.

With 20% down, lenders can sometimes be more flexible. This may include different qualification strategies and, in certain situations, slightly more borrowing flexibility. While it doesn’t automatically mean you’ll qualify for a higher purchase price, it can give you more room to structure your mortgage in a way that fits your goals.

For many first-time buyers, though, purchasing with less than 20% down is still an excellent path into homeownership.

Step 3: Complete a Full Mortgage Application

Once you’re ready, your mortgage broker (that’s me!) will typically have you complete a secure online mortgage application. This usually includes:

- Personal information

- Employment history

- Income details

- Current debts

- Down payment sources

- Consent for credit review

- Co-borrower details (if buying with spouse/partner/family)

Important for New Canadians

If you have not been in Canada for a full three years, some applications may display errors regarding address or employment history. Often these can still be worked through depending on the lender and program available.

Step 4: ID Verification & Credit Review

Mortgage brokers in Ottawa must comply with anti-fraud and identity verification regulations.

This often means using secure ID verification links, using your driver’s license or passport for verification, doing a credit bureau review, and having a final pre-approval discussion. Once complete, your broker can give you a much firmer buying range.

Step 5: Start House Hunting With a Realtor

Once you’re pre-approved, you can start shopping for homes with confidence, knowing your price range and what your monthly payments may look like. This is where having a trusted Ottawa realtor like Liam Swords really becomes valuable. They’ll help you book showings, write competitive offers, negotiate on your behalf, and walk you through local neighbourhood trends so you understand what you’re buying into. They can also review comparable sales to make sure you’re not overpaying, and guide you through conditions and key deadlines so nothing gets missed during the process.

If you’re considering a new construction home, it’s especially important to have representation in place early. Builders often have their own sales teams, so having your own realtor ensures you have someone looking out for your best interests from the very beginning.

Pick the Right Ottawa Community

Ottawa offers a wide range of communities depending on your budget and lifestyle.

Some buyers prioritize short commutes, good schools, and rental suite potential. While others may value walkability, access to transit, and future resale value.

Neighbourhoods can vary significantly in price, property taxes, condo fees, and home styles. That’s why it’s important to think not just about the house itself, but also how the area fits your long-term plans.

Step 6: Make an Offer on a Home

When you find the right property, your realtor helps prepare an offer. Typical items negotiated include:

- Purchase price

- Possession date

- Deposit amount

- Included appliances or items

- Conditions (financing, inspection, condo docs, etc.)

- The Deposit

Many Ottawa purchases involve an initial deposit (example: $10,000), though it varies by property and market. That deposit is usually held in trust by the real estate brokerage and later forms part of your total down payment.

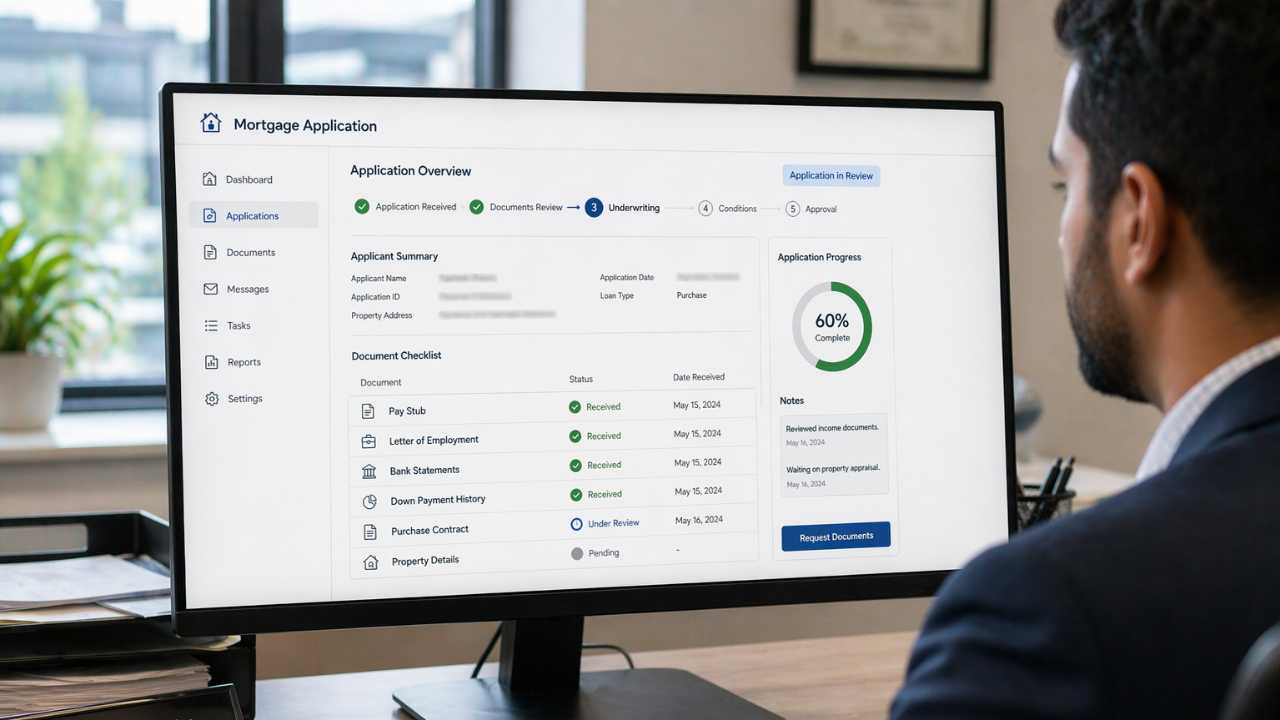

Step 7: Final Mortgage Approval

Once your offer is accepted, your mortgage moves from pre-approval to full approval.

Now the lender verifies:

- Income documents

- Most recent pay stubs

- Job confirmation if needed

- Bank statements

- Down payment history

- Purchase contract

- Property details

Important Tip

If documents are older, updated versions may be required. For example, they may need a more recent pay stub, updated bank statements, and proof of the deposit transfer. Responding quickly helps avoid delays.

Step 8: Home Inspection & Condo Document Review

During your condition period, you’ll usually complete due diligence.

Home Inspection

A professional home inspection is designed to give you a clear picture of the property’s condition before you fully commit. Inspectors can identify potential roof issues, estimate the age and condition of the furnace, and flag any electrical or plumbing concerns. They’ll also look for signs of moisture or water damage, along with general maintenance items that may need attention now or in the near future.

Even if no major problems are found, the inspection still provides valuable insight for first-time buyers. It helps you understand how the home functions, what to expect for ongoing maintenance, and where you may need to budget for repairs or upgrades over time.

Condo Document Review

If buying a condo or townhouse with condo fees, documents should often be reviewed for:

- Reserve fund health

- Pending special assessments

- Litigation risk

- Rules and bylaws

- Financial management

Step 9: Remove Conditions

Once financing, inspection, and condo review are satisfactory, you sign waivers removing conditions. At that point, the deal becomes firm, the seller cannot sell to someone else, and the buyer generally cannot back out without consequences.

This is a major milestone.

Step 10: Lawyer Appointment Before Possession

Usually about a week before possession, you meet with your real estate lawyer. You may need to bring:

- Government ID

- Proof of home insurance

- Certified funds or bank draft

- Remaining down payment funds

- Closing cost funds

Your real estate lawyer plays a key role in making sure everything is completed properly before possession. They handle the mortgage registration and title transfer, ensure the lender’s funds are received, and arrange for the seller to be paid. They also take care of the final adjustments, such as property taxes or prepaid expenses, so that both sides are treated fairly on closing.

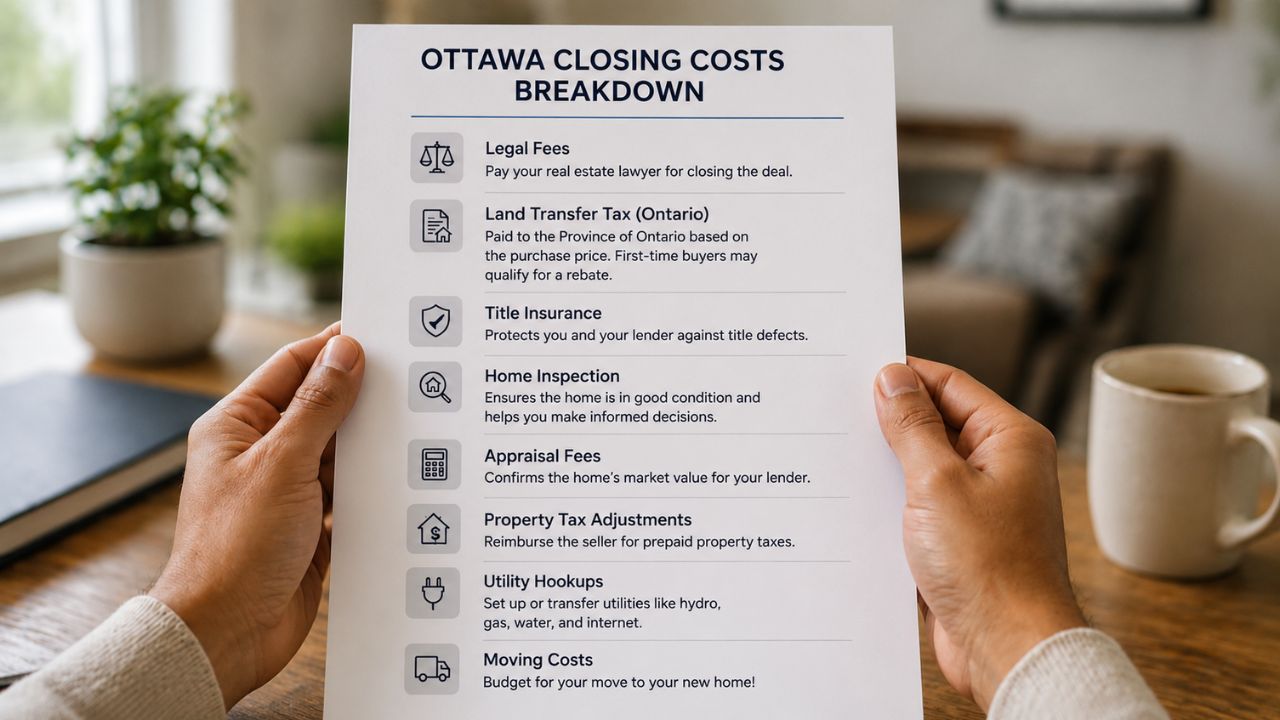

Step 11: Understand Closing Costs

Beyond your down payment, first-time buyers should budget for closing costs. A common planning range is often 1% to 3% of purchase price, depending on circumstances. These costs include items such as:

- Lawyer fees

- Land title registration fees

- Land transfer tax

- Mortgage registration fees

- Home inspection

- Appraisal fees

- Utility hookups

- Moving costs

- Property tax adjustments

Property Tax Adjustments Explained

This surprises many first-time buyers. If the seller already paid property taxes for the year, you may reimburse them for the portion covering the months you own the home. If they have not paid, adjustments may work in your favour. Your lawyer calculates this during closing.

Step 12: Possession Day – Get the Keys

On possession day:

- Funds are transferred

- Title work completes

- Realtor confirms release

- You receive keys

- You officially become a homeowner

Congratulations!

Smart First-Day Tip

Change the locks after taking possession.

Common First-Time Homebuyer Mistakes to Avoid

Many first-time buyers run into avoidable issues simply by not understanding the process upfront. Common mistakes I see include looking at homes before getting pre-approved, spending savings before closing, or taking on new debt before possession, all of which can impact your mortgage approval. Others miss document deadlines, underestimate closing costs, or ignore important findings during the home inspection. One of the biggest mistakes, though, is buying at the maximum amount a lender approves instead of choosing a monthly payment that actually feels comfortable for your lifestyle.

Why Work With a Mortgage Broker in Ontario?

A mortgage broker is like a search engine. Instead of having to go to each website one by one, it brings up multiple results all at once. Instead of going from bank to bank, A mortgage broker can help compare multiple lenders, explain options, and guide you through the process from start to finish. For first-time buyers in Ottawa, this can reduce stress and save time.

Need Help Buying Your First Home in Ottawa?

If you’re thinking about buying in Ottawa, or anywhere in Ontario, getting expert guidance early can make the process much easier.

Whether you need a mortgage pre-approval in Ottawa, down payment advice, or help understanding your options, the first step is simply starting the conversation. Contact me to have a conversation or to get started.