Buying your first home in Ottawa can feel overwhelming. I see it all the time with first-time buyers across Ottawa and Eastern Ontario. There are so many decisions happening all at once. Condo or freehold? Buy now or wait? Stretch your budget or keep payments lower?

Another question many buyers struggle with is whether they should buy a smaller home now or wait until they can afford something larger and closer to their long-term vision. Both options can make sense. The right choice depends on your finances, goals, and comfort level.

As a mortgage broker, I’ve worked with Ottawa buyers who were happy they entered the market sooner with a smaller property. I’ve also worked with buyers who felt more comfortable waiting until they were in a stronger financial position. The goal of this article is to help you understand which option may fit your situation best.

Buying a Smaller Home Now

Buying a smaller home now means purchasing something that fits your current budget, even if it is not your ideal long-term home.

In Ottawa, this often means:

- choosing a condo or stacked townhouse instead of a detached home

- buying farther from the downtown core

- considering older homes that may need cosmetic updates

- compromising on square footage or lot size

For many Ottawa first-time buyers, the goal is simply to enter the market sooner rather than waiting years for the “perfect” home.

A smaller home can allow buyers to:

- start building equity earlier

- keep monthly payments more manageable

- stop renting sooner

- benefit from future income growth while already owning property

This is especially important in Ottawa, where entry-level freehold inventory can still be competitive in many neighbourhoods.

For many Canadians, a first home is simply a starting point, not a forever home.

Waiting Until You Can Afford More

Waiting until you can afford more means delaying your purchase so you can potentially buy a larger home, save a bigger down payment, or qualify for a higher mortgage amount later.

Some Ottawa buyers choose this route because they want:

- a detached home instead of a condo or townhouse

- more space for future children

- a property in a specific school district or neighbourhood

- a home they can stay in for many years

Others simply want to strengthen their financial position first by paying down debt, increasing income, or building larger savings.

For some households, this approach makes sense. But waiting also comes with uncertainty because nobody knows exactly what home prices or mortgage rates will do in the future.

Ottawa’s market tends to be more stable than some Canadian cities, but affordability challenges still remain, especially for first-time buyers trying to save while paying high rent.

The Pros and Cons

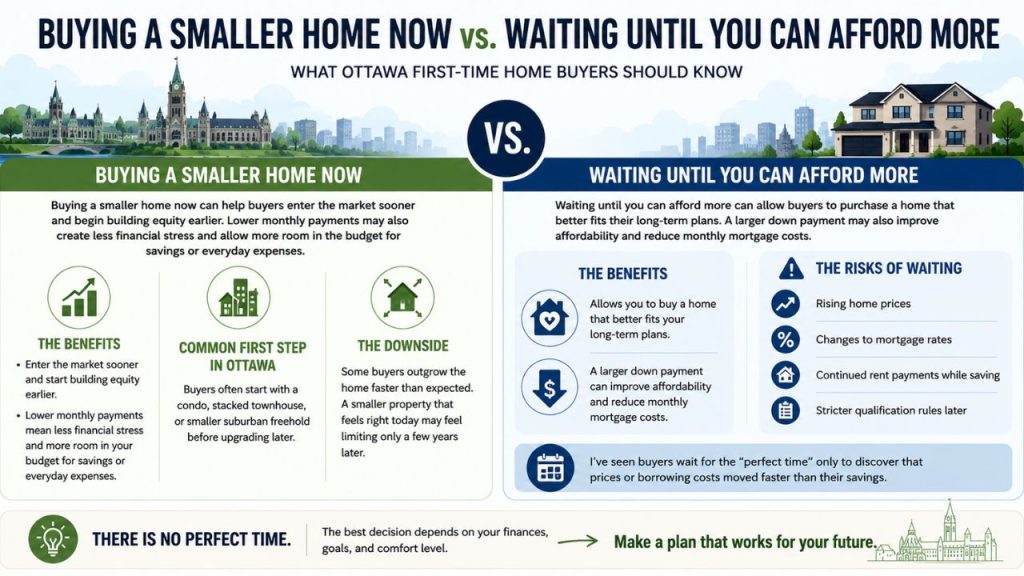

Buying a smaller home now can help buyers enter the market sooner and begin building equity earlier. Lower monthly payments may also create less financial stress and allow more room in the budget for savings or everyday expenses.

In Ottawa, I often see buyers start with a condo, stacked townhouse, or smaller suburban freehold before upgrading later.

The downside is that some buyers outgrow the home faster than expected. A smaller property that feels right today may feel limiting only a few years later.

Waiting until you can afford more can allow buyers to purchase a home that better fits their long-term plans. A larger down payment may also improve affordability and reduce monthly mortgage costs.

However, waiting also has risks, including:

- rising home prices

- changes to mortgage rates

- continued rent payments while saving

- stricter qualification rules later

I’ve seen buyers wait for the “perfect time” only to discover that prices or borrowing costs moved faster than their savings.

Which Option Is Better for First-Time Buyers?

Every buyer’s situation is different.

Buying a smaller home now may make sense for buyers who:

- want to enter the market sooner

- expect their income to grow later

- want to stop renting

- prefer lower monthly costs and flexibility

This often works well for:

- younger professionals

- newcomers to Canada

- first-time buyers early in their careers

- buyers with stable long-term employment growth

Waiting until you can afford more may make more sense if buying today would stretch your budget too aggressively or if you are already close to reaching your savings goals.

What matters most is making sure your monthly budget still feels comfortable after you move in. Just because a lender approves you for a certain amount does not necessarily mean you should spend the maximum available budget.

The Mistake Many First-Time Buyers Make

A pattern I’ve noticed over the years is that many buyers feel pressure to purchase their dream home immediately. That pressure can cause people to delay buying for years because they believe anything less than a perfect home is the wrong decision.

In reality, many homeowners build wealth gradually. They start with something smaller, build equity over time, and upgrade later as their financial situation improves.

At the same time, some buyers become so focused on “getting into the market” that they ignore how tight their monthly budget may become afterward.

The goal is finding a balance between entering the market and maintaining financial stability.

How a Mortgage Broker Helps You Decide

A mortgage broker can help you compare different purchase scenarios based on your income, down payment, debts, and monthly comfort level.

Sometimes Ottawa buyers are surprised to learn they qualify for more than expected. Other times, they realize a smaller purchase may allow them to live much more comfortably month to month.

Looking at real numbers often makes the decision much clearer.

I can also help buyers understand:

- what monthly payment feels realistic

- how much condo fees impact affordability

- how Ottawa property taxes affect qualification

- whether a condo, townhouse, or detached home makes the most sense financially

- how new first-time buyer programs and longer amortizations may help affordability

The important thing is making a decision based on your own finances, goals, and comfort level rather than trying to perfectly time the market.

If you’re trying to decide between buying a smaller home now and waiting until you can afford more, the best next step is understanding what your mortgage options actually look like. Contact me and we can compare both scenarios using real numbers so you can make a confident decision for your future.