Buying your first home in Ottawa has become more challenging over the past few years. Between higher home prices, stricter mortgage qualification rules, and rising living costs, many first-time buyers are finding it harder to qualify on their own.

That’s why more buyers are exploring options like using a co-signer or buying with a co-borrower.

At first glance, these two options can seem very similar. Both can help you qualify for a larger mortgage and improve your chances of getting approved. But legally and financially, they are very different arrangements.

As an Ottawa mortgage broker, this is something I spend time helping clients navigate. And choosing the wrong structure can create major problems later if you don’t fully understand how it works.

Here’s what Ottawa first-time homebuyers should know about co-signers vs co-borrowers in Ontario.

What Is a Co-Signer?

A co-signer is someone who helps strengthen your mortgage application without necessarily becoming a true owner of the home in the way most buyers think of ownership.

In many cases, this is a parent or close family member who agrees to support your mortgage application because your income, employment history, or credit isn’t quite strong enough on its own. Mortgage lenders may require a co-signer when a borrower does not fully qualify independently.

The co-signer becomes legally responsible for the mortgage debt if you stop making payments. That means the lender can pursue them for missed payments, even if they never contributed to the purchase or lived in the property.

In Ottawa, this is especially common among:

- Younger buyers entering the market for the first time

- Buyers with strong future income potential but limited current income

- New Canadians with shorter Canadian credit histories

- Buyers trying to qualify in higher-priced neighbourhoods

Depending on the lender and legal structure, a co-signer may need to appear on title temporarily, even if they are not intended to have a true ownership interest in the home.

What Is a Co-Borrower?

A co-borrower is someone who purchases the home with you.

They share both the mortgage and ownership of the property. Their income, debts, credit score, and assets are all included in the mortgage qualification process.

This is most common with:

- Spouses or partners buying together

- Siblings purchasing a home jointly

- Family members combining income to afford a property in Ottawa

- Friends purchasing together in some cases

With a co-borrower arrangement, both people usually appear on title and both share ownership of the home. A co-borrower is not simply “helping you qualify.” They are buying the property alongside you.

The Pros and Cons of a Co-Signer

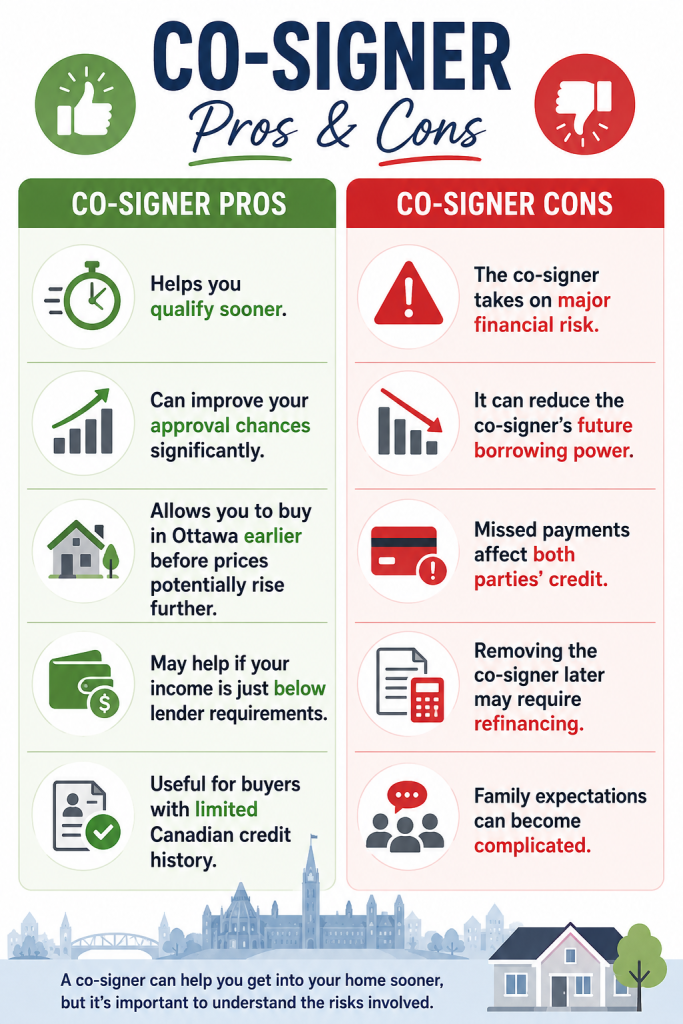

Co-Signer Pros

- Helps you qualify sooner

- Can improve your approval chances significantly

- Allows you to buy in Ottawa earlier before prices potentially rise further

- May help if your income is just below lender requirements

- Useful for buyers with limited Canadian credit history

Co-Signer Cons

- The co-signer takes on major financial risk

- It can reduce the co-signer’s future borrowing power

- Missed payments affect both parties’ credit

- Removing the co-signer later may require refinancing

- Family expectations can become complicated

One thing many buyers don’t realize is that co-signing can also impact Ontario first-time buyer incentives and rebates depending on how ownership is structured. For example, if a co-signer is added to title, it can sometimes affect land transfer tax rebate eligibility.

That’s one reason proper planning matters so much in Ontario.

The Pros and Cons of a Co-Borrower

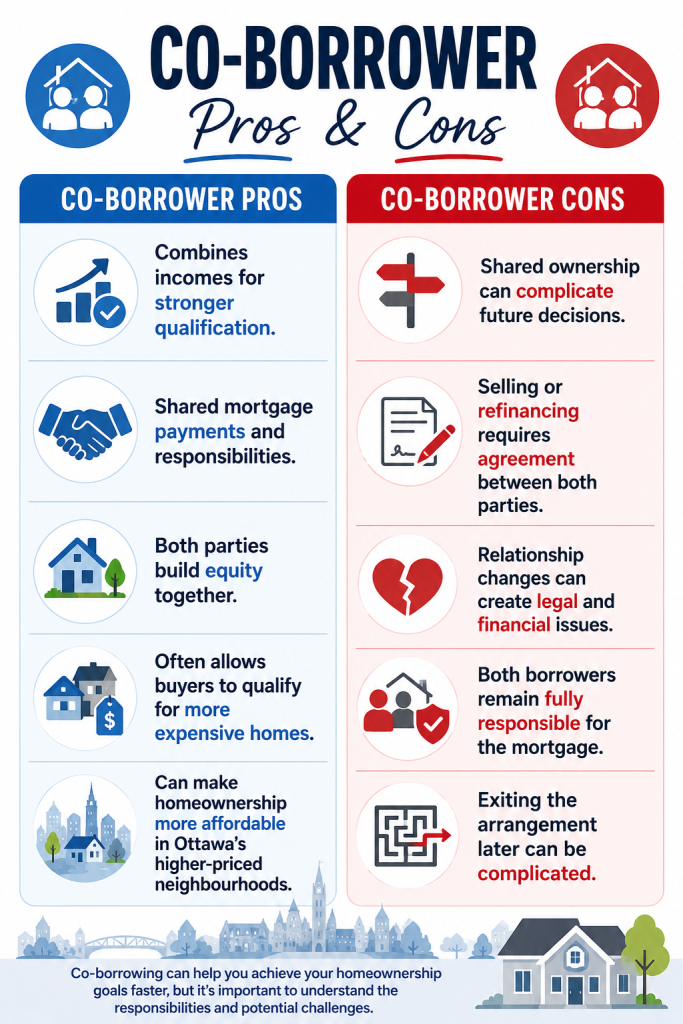

Co-Borrower Pros

- Combines incomes for stronger qualification

- Shared mortgage payments and responsibilities

- Both parties build equity together

- Often allows buyers to qualify for more expensive homes

- Can make homeownership more affordable in Ottawa’s higher-priced neighbourhoods

Co-Borrower Cons

- Shared ownership can complicate future decisions

- Selling or refinancing requires agreement between both parties

- Relationship changes can create legal and financial issues

- Both borrowers remain fully responsible for the mortgage

- Exiting the arrangement later can be complicated

A co-borrower arrangement works best when both parties have aligned long-term goals and clear expectations.

Which Option Makes More Sense in Ottawa?

There isn’t one correct answer for everyone.

A co-signer may make more sense if you intend to purchase alone, only need a small boost to qualify, expect your income to rise soon, or have a family member who is willing to help temporarily.

A co-borrower may make more sense if you’re purchasing with a partner, plan to live there together long term, want to split ownership and costs, and if both parties are equally invested financially.

In Ottawa specifically, I’m seeing more buyers explore co-buying arrangements simply because affordability has become more difficult for single-income households.

The Mistake Many Buyers Make

Here are some important questions to ask:

- How easy will it be to remove the co-signer later?

- What happens if one co-borrower wants to move?

- How will this affect future borrowing?

- What happens if relationships or financial situations change?

Just because a lender approves something doesn’t mean it’s the best long-term strategy. The structure of the mortgage matters almost as much as the approval itself.

How an Ottawa Mortgage Broker Can Help

This is where working with an experienced Ottawa mortgage broker can make a huge difference.

When I help clients compare co-signer vs co-borrower options in Ontario, I’m looking beyond just approval numbers. I’m looking at:

- Your long-term plans

- Future refinancing options

- Potential risks for everyone involved

- Ontario rebate and tax implications

- Exit strategies later on

- Whether there may be simpler alternatives

Sometimes buyers assume they need a co-signer when they actually qualify another way. Other times, buyers choose co-borrowing without fully understanding the legal and financial responsibilities involved.

My goal is to help you understand all your options clearly before making a decision.

Next Steps

Both co-signers and co-borrowers can help Ottawa first-time homebuyers get into the market sooner. But they are not interchangeable.

- A co-signer mainly helps support the mortgage application.

- A co-borrower shares ownership and responsibility for the home itself.

The right choice depends on your financial situation, your relationships, and your long-term goals.

If you’re trying to figure out which option makes the most sense for your situation, reach out and I’d be happy to walk you through your options.